Outpatient prescription drugs account for about 10 percent—$259 billion in 2010—of total U.S. health spending. Expiring patents on many of the most commonly prescribed drugs have helped slow the rate of spending growth in recent years, but drug spending is likely to accelerate again as new drugs come to market. Other developed countries typically pay much lower prices for brand-name drugs than the United States. However, health systems in other industrialized nations operate much differently than the U.S. system. While some approaches used in those nations may not easily translate here, other tools offer potential lessons in slowing prescription drug spending growth.

Two approaches from other national systems that could achieve savings in the United States are reference pricing, as used in Australia and elsewhere, and the application of comparative-effectiveness and cost-effectiveness research, as done in the United Kingdom. With appropriate modifications to fit the U.S. context, both approaches could increase the use of generic drugs and less-expensive brand-name drugs, helping to constrain spending growth. In particular, reference pricing—an approach where a payer sets payment for a group of similar drugs using a benchmark based on a lower-priced option—could increase consumer incentives to select less-expensive alternatives. Similarly, an approach that bases formulary placement and cost-sharing tiers on scientific assessments of the clinical value of competing drugs offers the potential both to increase acceptance of cost management by patients and physicians and to improve health outcomes.

- Prescription Drug Spending Growth Modest for Now

- Potential Cost Savings on Prescription Drugs

- Increasing Use of Generics and Other Cost-Effective Drugs

- Reference Pricing

- Reference Pricing Options in the United States

- Comparative Effectiveness, Cost Effectiveness and Value Pricing

- Using Evidence to Guide Decisions

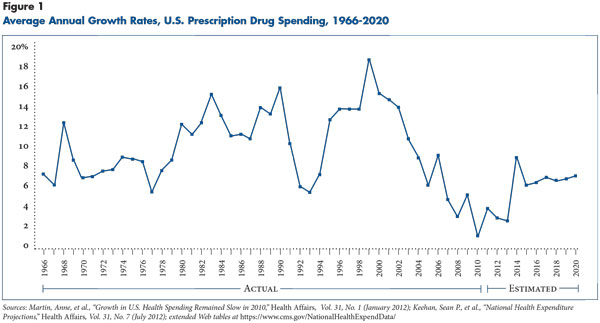

Prescription Drug Spending Growth Modest for Now

Total spending on prescription drugs purchased at U.S. retail pharmacies in 2010 was $259 billion, representing 10 percent of total national health expenditures.1 Beyond their cost, prescription drugs contribute to health care spending in other ways. Obtaining a prescription for a drug requires diagnosis of a medical condition and is normally associated with other health care services linked to that condition, including at least one physician visit to receive the prescription. On the other hand, successful adherence to drug regimens may mean better health and avoidance of health services associated with deteriorating medical conditions and possible cost savings.

The rate of drug spending growth reached a historically low level of 1.2 percent in 2010, with an average annual growth rate of about 3.7 percent between 2006 and 2010—slower than growth in overall health spending. By contrast, drug spending grew faster than overall spending for the previous several decades, with average growth rates between 11 percent and 13 percent from the 1980s through the mid-2000s (see Figure 1). But there is no guarantee that slower growth will continue. Federal actuaries project that prescription drug spending growth will accelerate modestly over the next decade and again exceed overall spending growth, in part because of higher use resulting from expected coverage expansions.2

From the individual consumer’s perspective, the financial burden associated with drug costs has moderated somewhat, corresponding to both slower growth in total drug spending and lower patient cost sharing associated with generic drug use. In 2008, only about 5 percent of Americans younger than 65 lived in families where out-of-pocket drug costs accounted for more than 5 percent of family income. But, about 25 percent were in families where out-of-pocket drug costs represented half of total out-of-pocket health costs.3

The biggest factor in slower drug spending growth has been the increased use of generic drugs (see box below for more about brand and generic drugs). Since the mid-2000s, many of the most-prescribed brand-name drugs have lost patent protection, and many more will do so in the next several years. Aggressive generic substitution has helped bring down total costs. At the same time, relatively few new drugs with the potential for large market shares and high costs have been approved in recent years. As of 2011, 80 percent of prescriptions were filled by generic drugs—up from 63 percent in 2006. Generics, however, accounted for only 27 percent of all drug spending.4 Projections for a return to faster drug spending growth reflect in part an expectation that use of generics will level off and that more new drugs will be approved in the next decade.

Brand and Generic Drugs in the United States

Brand-name, single-source drugs are under patent protection and can be sold only by the manufacturer that developed and was awarded approval to sell the drug. In nearly all cases, these drugs are sold under a brand name and are typically referred to as brand-name drugs. A multiple-source drug is one that is no longer under patent protection, and both brand-name and generic versions are available from a variety of manufacturers.

In general, a generic drug receives approval by the Food and Drug Administration (FDA) as bioequivalent to the original brand-name drug. The first manufacturer to receive approval to sell a generic version of a drug generally receives a six-month exclusivity arrangement and serves as the sole competitor to the original manufacturer during that period. After six months, other approved manufacturers may enter the market. This broader competition usually leads to much lower prices.

In many cases, the original manufacturer will continue to market the drug under the original brand name in competition with generic versions of the drug—possibly including generic versions made by the original manufacturer—but at a higher price. In some cases, a competing manufacturer may give a generic drug its own brand name, typically referred to as a branded generic. An example is Budeprion, a version of the antidepressant bupropion, which was first marketed under the brand name Wellbutrin. Branded generics are often priced somewhere between generics and the version with the original brand name.

Potential Cost Savings on Prescription Drugs

Among the ways to reduce spending on prescription drugs are shifts in utilization from brand-name drugs to generics and from more-expensive to less-expensive brand-name drugs. The competition among multiple generic versions of the same chemical entity means that the cost of a generic prescription averages about one-fourth that of an equivalent brand-name prescription.5 Increased use of generic drugs can potentially reduce overall drug spending in a way that benefits both payers and patients as long as they are safe and equally effective alternatives.

Direct generic substitution for the same chemical entity is the easiest step, because the alternative drugs are determined to be safe, effective and equivalent by the FDA approval process. The more difficult step for patients and prescribers, as well as payers, is substitution among a set of similar drugs that have each passed safety and efficacy hurdles. Therapeutic substitution, the use of a generic alternative in place of a different chemical entity in the same drug class, lacks any FDA guarantee of equivalency. Although considerably more challenging than generic substitution, the potential for cost savings from therapeutic substitution is much greater.

An analysis sponsored by the generic drug industry found that the existing use of generic drugs resulted in about $193 billion in savings in 2011.6 The Congressional Budget Office has estimated that use of generic drugs in Medicare Part D generated $33 billion in savings in 2007—costs would have been 55 percent higher without generics.7

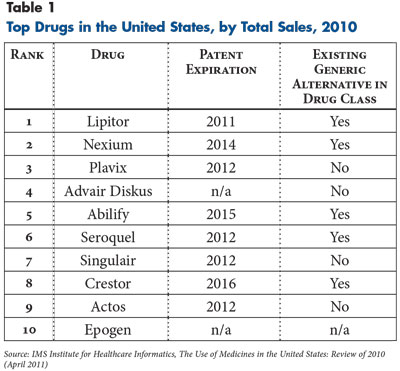

Various studies have demonstrated additional savings from greater use of generics because they facilitate further therapeutic substitution as well.8 The savings opportunity from greater generic use is evident from the top 10 drugs, based on total costs in 2010. Five of the top 10 drugs are in drug classes where there was already a generic alternative in 2010 (see Table 1). For example, both Lipitor and Crestor are statins used to treat high cholesterol—a class where three generic drugs were available in 2010 and where a generic version of Lipitor became available in 2011. This drug class offers opportunities for therapeutic substitution. Furthermore, another four of the top drugs—Seroquel, Plavix, Singulair and Actos—will be off patent and have generic alternatives by the end of 2012. Not only will these patent expirations create easier means for savings through generic substitution, but several will open new opportunities for therapeutic substitutions. The only drugs among the top 10 without a foreseeable opportunity for generic competition are Advair Diskus, an inhaler used to treat asthma or chronic obstructive pulmonary disease, and Epogen, a biologic used to treat anemia. In both cases, the patent situation is more complicated.

Biologic drugs—derived from living organisms rather than chemical compounds—are likely to be a mounting source of cost growth. In fact, six of the drugs in the next 10 ranked positions by sales are biologics like Epogen. Competition relies on implementation of approval pathways for follow-on biologics or biosimilars, which could serve a role akin to generic drugs. But true price competition will rely on either FDA certification of interchangeability between the original biologics and the follow-on products or acceptance of the new products as legitimate alternatives by clinicians and patients.

Inreasing Use of Generics and Other Cost-Effective Drugs

In the past decade, purchasers and payers have encouraged enrollees to use less-expensive drugs. Broader use of both generic substitution and therapeutic substitution has contributed to slower growth in drug spending and may help maintain these trends.

The U.S. health system has typically achieved good results in terms of generic substitution for chemically equivalent alternative prescription drugs. In 2010, about 80 percent of patients started using the generic version of a drug within six months after patent expiration of the originator drug and entry of the first generic version on the market. By the end of 12 months, the generic share typically approached 100 percent. These levels are considerably above those achieved just a few years ago.9

But, the transactions involved in a drug purchase entail many parties, including the patient, prescribing physician, pharmacist, health plan, pharmacy benefit manager (PBM) and pharmaceutical manufacturer (see box below for an overview of drug purchasing and pricing). And, the complexity makes change more difficult.

The high use of generics is facilitated by a combination of state laws on substitution and incentives offered by health plans. Most states permit pharmacists to substitute a generic drug for the chemically equivalent brand-name drug, with some restrictions. For example, some states require consent from the patient before making a substitution, and all states have a means for the physician to require that a prescription be filled with a brand-name version of a drug.12 At least one study found that state Medicaid programs achieved a 98 percent generic share for one particular generic drug within six months when patient consent was not required, compared with less than one-third after six months (about 85 percent after 12 months) in states requiring patient consent. Average prices—across brands and generics—also declined less rapidly in states requiring consent.13

Approaches used by health plans and PBMs to manage costs, many of which take advantage of the electronic point-of-sale system, aim at both price and utilization. Some of the more common tools include:

- Price discounts and rebates. PBMs typically use the volume of prescriptions managed to obtain discounts from manufacturers, especially for brand drugs in competition with other brand therapies. Because PBMs do not purchase drugs directly, the discounts are mostly received in the form of manufacturer rebates based on volume or market share. Rebate amounts for particular drugs are proprietary information, but they are estimated to average about 20 percent for the top-selling brand drugs.

- Tiered formularies. Plans use tiered formularies to create an incentive for enrollees to use generics or less-expensive brand drugs. Drugs on a plan’s formulary are typically placed on tiers—for example, generic, preferred brand and nonpreferred brand—with different cost-sharing amounts for each tier. Drugs that are off formulary may be obtained by requesting an exception based on a physician’s recommendation or by paying the full cost out of pocket.

- Utilization management tools. Plans use such tools as prior authorization, where the prescribing physician must offer justification for use and the plan must grant approval before a particular drug is dispensed; or step therapy, where the patient must try and fail to achieve desired outcomes with a less-expensive drug before a more-expensive drug may be dispensed.

Health plans find various strategies effective in encouraging enrollees to make generic substitutions for the chemically equivalent drug. First, plans may leave the brand version off formulary, meaning it would be covered only if the plan grants an exception. Second, plans may include the drug on formulary, but dispense it only with prior authorization or under a step-therapy requirement. Finally, plans may place the brand version of the drug on a nonpreferred tier with higher cost sharing required, thus creating a financial incentive for the patient to request the generic version. In 2011, the typical cost-sharing amounts for private plans were $49 for a nonpreferred tier drug vs. $10 for the generic tier, while Medicare Part D plans have a wider gap between tiers—$78 vs. $7.14 Some health plans also use educational campaigns aimed at either physicians or patients to encourage more use of generic drugs.15

Therapeutic substitution relies on the same tools but faces more challenges. Substitution by pharmacists is not generally an option in the United States without a new prescription from a physician.16

Research has shown that patient and physician perceptions and preferences limit the maximum reach of generic drugs—whether direct substitution or therapeutic substitution. Some patients believe that brand-name drugs are safer than generic drugs, and older patients, those with lower incomes and those with self-reported poor health status are more likely to indicate concerns.17 Despite perceived concerns, the clinical literature consistently supports the equivalency of brand and generic versions of nearly all drugs.18

Physician preferences matter as well, although e-prescribing has some potential to change this.19 Furthermore, physicians often fail to discuss cost-related issues with their patients and are typically unaware of the cost of drugs.20 Even when physicians understand the importance of taking costs into account in prescribing, they often lack both time and needed information. In many cases, the result is that the drug selected for the patient’s original prescription is based primarily on clinical considerations—though perhaps influenced by patient preferences and marketing by the manufacturers—but not necessarily the most cost-effective choice.21

Drug Purchasing and Pricing in the United States

A drug may only be dispensed after a physician or other authorized clinician writes a prescription. The prescribing clinician often does not take into account the drug’s cost or its status on a health plan’s formulary. Unlike their counterparts in some other countries, U.S. pharmacists may dispense a chemically equivalent generic drug instead of a brand-name drug without a new prescription. Under the electronic point-of-sale system in place for most transactions, pharmacists receive notification of whether a particular drug is covered by a health plan, but a switch to a therapeutically similar drug—unlike a switch to a generic—requires the clinician to change the prescription. Electronic prescribing (e-prescribing) may allow clinicians to learn a drug’s status on a plan formulary, including the patient cost sharing and any restrictions at the time they write a prescription. Although use of e-prescribing by physicians is growing, evidence suggests that much of the tool’s potential is not yet being realized because of shortcomings in coordination.10

Drug coverage for most Americans is administered by health plans in conjunction with a PBM. The PBM does not take possession of the drugs, other than under mail-order purchases. PBMs manage pharmacy transactions and provide overall benefit management, including maintaining formularies, obtaining price discounts, organizing pharmacy networks and administering quality assurance programs. As of 2011, about 85 percent of prescriptions directly involved a third-party payer, such as a health plan.11 As recently as 1990, most Americans paid for their prescription out of pocket and then filed a claim with their insurer. Since then, it has become standard practice for insurers to process the claims at the point of purchase. On a real-time basis, the claim is reviewed to determine the drug’s coverage status and any restrictions. The pharmacy collects the appropriate copayment or coinsurance from the patient and receives the additional payment from the insurer.

Because the drug itself is purchased from a pharmacy that obtains the drug either from a manufacturer or through a wholesaler, prices involve a mix of retail transaction prices, discounts negotiated with pharmacies, and discounts in the form of rebates paid by the manufacturer to the health plan or PBM.

Reference Pricing

One tool used infrequently in the United States, but more common in some other nations, is reference pricing. Pioneered by Germany in 1989, reference pricing, in many variations, is used mostly in countries with national or provincial health systems, including Australia, Belgium, Germany, Hungary, Italy, the Netherlands, New Zealand, South Africa, Spain and the Canadian province of British Columbia.22 The concept of reference pricing is that a payer, such as a private health plan or a national health system, sets payment for a group of similar drugs based on a benchmark. The benchmark, or reference price, for a group of drugs may be determined in a variety of ways, such as the price of the lowest-cost drug in the group or some type of average price. The consumer pays any difference between the reference price and the price of the prescribed drug.

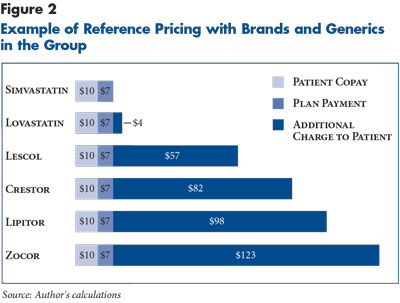

For example, in a group of six drugs used to treat high cholesterol, retail prices might range from $17 to $140 for a one-month supply of the drug (see Figure 2). If all six drugs are considered equally satisfactory treatments, then the reference price in this example would be set at the price of simvastatin (the generic version of Zocor), and the cost of that drug is divided between a $10 patient copayment and $7 paid by the plan. For any other drug in the group, the patient pays the additional amount above $17. Thus, a patient selecting Zocor would pay a total of $133 out of the retail price of $140. By contrast, if Zocor were on a nonpreferred tier, the copayment paid by the patient is $49 in an average plan.

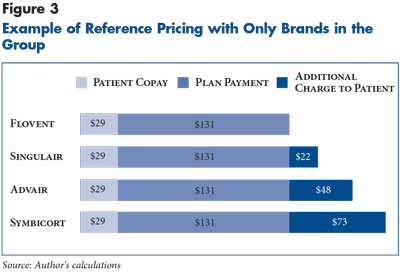

In a drug group where only brand drugs are available, the comparisons would be somewhat less extreme. Using several asthma control medications (see Figure 3), the reference price would be set based on Flovent, the least-expensive drug in the group, with a $29 copayment and a plan payment of $131. The total payment for users of the alternatives would range from $51 to $102.

The word “pricing” may be misleading in a setting other than a national health system, because a health plan or other payer uses reference pricing to set the amount to be paid for the drug, not the manufacturer’s price for the drug. But even in national systems, some see the advantage of reference pricing over direct price regulation is that it sets a payer’s payment amount, rather than directly regulating or setting market prices. Therefore, reference pricing serves more as a form of value-based purchasing where the payer sets the maximum amount it will pay, sensitizing patients and physicians to the relative prices of competing drugs. Patients and physicians can then evaluate price against the benefits of different drug therapies. Patients can pay extra for drugs sold above the reference price if they believe the potential benefit is worth it.23 Manufacturers also may choose to modify market prices in response to these influences.

Generic Reference Pricing

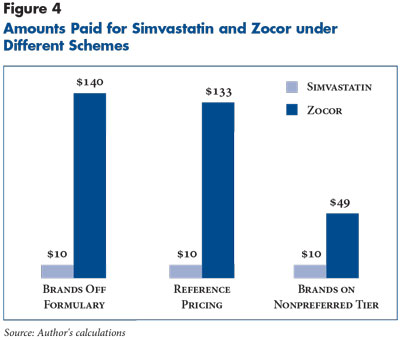

The simpler version of reference pricing is generic reference pricing, which applies only to a set of drugs that are chemically equivalent. For example, one reference price would be used for all versions of simvastatin, a drug used to treat high cholesterol, including the branded version, Zocor, and all generic equivalents. As such, reference pricing is a variant of other tools to encourage generic substitution, falling between leaving the brand version of a drug off formulary and placing the brand version of a drug on a nonpreferred tier. Using the drugs from the previous example, a patient selecting Zocor over generic simvastatin would pay $140 if the plan offered no coverage, $133 under reference pricing—$10 generic copayment plus the $123 price differential—but only $49 if Zocor is on a nonpreferred tier (see Figure 4).

Use of generic reference pricing among large employers in the United States is limited. One recent survey found that small fractions—about 1 percent—of covered workers are in plans with generic reference pricing.24 Another survey found evidence of somewhat more use, reporting that about 10 percent of large employers (at least 1,000 employees) use the strategy.25 Some Medicare Part D plans experimented briefly with generic reference pricing, but the Centers for Medicare and Medicaid Services (CMS) eliminated the option in 2009 because of patient advocates’ concerns about confusion and lack of transparency in pricing.26

Most research shows that generic reference pricing is associated with a significant increase in the generic share of drug utilization and a decrease in drug prices for the products subject to the policy. Furthermore, significant savings were shown in the first years after the policy was applied to a particular group of drugs. Some exceptions were found to the overall pattern in cases either where brand drug prices were lowered to meet the reference price or where new dosages or formulations entered the market and offered a potentially superior product to the generic version of the original drug.27

Therapeutic Reference Pricing

Therapeutic reference pricing differs from generic reference pricing in terms of the set of drugs compared. The frame of reference is expanded from a set of drugs that are bioequivalent to a broader set of drugs that are therapeutically equivalent—for example, all statins used to treat high cholesterol. Not all drug classes may be suitable for the stronger incentives embedded in reference pricing, especially classes where clinical evidence on interchangeability of drugs is limited. Furthermore, broader or narrower definitions of a drug class may be controversial, but the general principle is typically to include a set of drugs that physicians consider appropriate for substitution for most patients.

Research on the effectiveness of therapeutic reference pricing shows consistent and significant drops in prices—and substantial savings—for groups of drugs where it has been used.28 There is limited research looking at adverse health effects from reference pricing, with almost all existing studies (mostly from Canada) finding no effects, and only one (from Germany) showing ambiguous results. Another study examined a limited literature comparing the effectiveness of reference pricing vs. tiered formularies. Both approaches were found to be effective in altering drug use and reducing drug costs but with a slight edge to reference pricing.29 Therapeutic reference pricing has been prominent in Australia (see box below for more about Australian practices). The Australian reference pricing system affects both the price paid for a drug by the national health system and patient cost sharing. In this regard, it differs from applications in the United States, where no easy mechanism exists for a single health plan to influence the manufacturer’s price. In Australia, although prices are not directly regulated, manufacturers tend to set prices close to the reference price. Most drugs have prices set at the reference price or slightly above, with 63 percent of prescriptions dispensed at the reference price in 2006 and the rest at a premium price.32 A case study of a state employee health plan program in the United States helps to illustrate the potential savings achieved.33 In this case, reference pricing was used for proton pump inhibitors (PPIs), a class of drugs used to treat gastrointestinal issues. The over-the-counter version of generic omeprazole established the reference price, and the cost to consumers for all other PPIs was the additional cost above the over-the-counter version.34 Following the policy change, the average price per day for all filled prescriptions was lower by 38 percent, net costs for the health plan decreased by about 50 percent, and out-of-pocket costs for plan enrollees also were lower.

Reference Pricing Options in the United States

In the United States, reference pricing is likely to be used as part of an insurance benefit design that offers an incentive for plan enrollees to select one drug over another—potentially a stronger incentive than in benefit designs with tiered cost sharing. Many other nations use reference pricing as both a benefit design and a purchasing tool in a national drug purchasing strategy. In nations such as Australia, one reference price decision may be made for a national health system. In the United States, independent decisions would be made by different payers that cannot individually easily influence the price paid to the manufacturer.35

Because payments are made to the pharmacy, not the manufacturer, use of a reference price to set the total price paid for the drug would inappropriately penalize the pharmacy. Payers could try to use a reference pricing framework in rebate negotiations with manufacturers, but this process is substantially different from the type of negotiation that occurs in Australia over a large share of all drugs used in the country. If many large purchasers applied reference pricing, however, manufacturers of the higher-priced drugs might have an incentive to lower prices for those drugs.

Private-sector health plans could consider generic or therapeutic reference pricing as a means of establishing a different incentive structure to encourage their enrollees to use generic drugs or less-expensive brand drugs. In reference pricing, cost-sharing incentives will vary by drug. Instead of charging the same cost sharing for all nonpreferred drugs, the most expensive drugs will have the highest cost sharing.

Plans have a direct financial incentive to experiment with different tools that encourage the use of less-expensive drugs without the need to increase overall costs for plan enrollees. Switching to a generic drug should bring down costs for both the payer and the enrollee. As health cost pressures continue to increase, the incentives to find cost savings that go beyond shifting costs to enrollees will only increase. Countervailing pressure may result if enrollees perceive that access to their choice of drugs will be curtailed by this approach.

In Medicare, private Part D plans currently are denied authority to use reference pricing, although they are permitted to leave drugs off formulary or place them on nonpreferred tiers with higher cost sharing. CMS, however, could use administrative authority to modify current policy and give plans more ability to employ either generic or therapeutic reference pricing. The Congress also could permit or mandate some use of reference pricing. To avoid the issues raised by consumer advocates in 2009, CMS would need to ensure that the online tool used by Medicare beneficiaries to compare prices across different plans accurately displays the out-of-pocket costs under reference pricing.

In either private insurance or Medicare settings, the use of reference pricing brings up technical issues:

- What is the basis for calculating the reference price? Is the consumer liable for the entire difference above the least-expensive option, or is the reference price based on an average of several lower-cost options?

- What factors are taken into account in establishing a reference price? In the simplest application, the reference price is the lowest for all drugs in a class, but the reference price could be set higher to include a drug that is clinically superior and where the higher price is commensurate with the added value. Alternatively, the lowest-price drug could set the reference price, but cost sharing for the clinically superior drug could be set lower than under full reference pricing.

- What drugs are combined in a group to form the basis for a reference price? In most current applications, the set of drugs includes those where clinical evidence suggests that most clinicians should be willing to substitute the drugs for most patients. For example, ACEs and ARBs are viewed by some clinicians as substitutable and thus could be viewed as one group of drugs to treat hypertension. But other clinicians point to fewer side effects for ARBs and would prefer easier access to those drugs, which tend to be more expensive. Health plans would need to decide whether clinical evidence supports the larger, combined class. Small drug groups also could be considered to target more narrowly so-called “me too” drugs with little therapeutic advantage from similar, less-expensive drugs.

For pure generic substitution, reference pricing is likely to have only a modest impact because generic use rates are already more than 90 percent in most cases.36 Reference pricing, however, could provide greater flexibility for patients willing to pay the additional cost for the brand alternative, compared to excluding the latter from formularies.

Encouraging therapeutic substitution among competing alternatives in a particular drug class through the use of reference pricing brings more opportunity for savings but raises more issues. Based on clinical evidence, some drug classes are more suitable than others for therapeutic substitution. For example, many clinicians see little reason to prefer one proton pump inhibitor for gastrointestinal ailments over another, while many are reluctant to switch a patient from one antidepressant or antipsychotic drug to another.37 These same concerns exist under tiered cost sharing, but raising the cost differential, where one or more generics in a class is available to substitute for on-patent brands, may heighten concerns for some doctors and patients.

The situation is somewhat different in a drug class where all competing alternatives remain on patent with no generic available. If all drugs are considered reasonably close substitutes, the reference price might be established by the least-expensive therapy. In some such classes, the cost of the therapeutic alternatives may be only modestly higher than the preferred drug. Use of reference pricing could make these alternatives less expensive to the patient than under tiered cost sharing, where the alternatives are placed on a nonpreferred tier.

Therapeutic reference pricing may generate consumer resistance if viewed as restricting access to their drugs of choice. Most plans today already employ formularies that may impose limitations on access to drugs; for some, access to a drug at the reference price may increase access compared to a situation where the same drug is off formulary. But, compared with plans with tiered formularies, use of reference pricing would often increase the consumer’s cost above that of a drug on a nonpreferred tier. Consumer concerns about reduced access or increased cost may be addressed by assurances that all formulary decisions would be based on the best available clinical evidence. For some drug classes, for example, recent studies have found that older, less-expensive therapies are more effective than newer, more-expensive drugs. An additional protection for consumers, for both reference pricing and tiered cost sharing approaches, would come from a fair and timely process to obtain exceptions when specific clinical reasons, such as an adverse reaction to the drug available at the reference price, justify use of a different drug.

Some observers also raise concerns that limiting access to new, more-expensive products, whether through tiered cost sharing or reference pricing approaches, may cut into the revenue and profits of pharmaceutical manufacturers, thus reducing investment in research and development and deterring innovation. Although there is little empirical evidence to support this concern, it is a critical consideration. One study found no significant effect on profitability and innovation in the pharmaceutical industry.38 The combination of reference pricing or other formulary tools with good comparative-effectiveness information would be vital to ensure that the value of a new drug is recognized, but that its price is commensurate with this added value.

Comparative Effectiveness, Cost Effectiveness and Value Pricing

An additional step to slow prescription drug spending growth would take the incentives for therapeutic substitution created by either tiered cost sharing or reference pricing approaches and pair them with evidence on comparative effectiveness or cost effectiveness.39 Some consumers and their physicians are skeptical that purchasers and payers have patients’ best interests in mind when creating incentives to obtain some drugs in preference to others. Linking formulary decisions more closely to research evidence can potentially add credibility.

Comparative effectiveness and cost effectiveness have been subjects of considerable debate by U.S. policy makers in recent years. Most recently, the 2010 Patient Protection and Affordable Care Act (PPACA) allocated considerable new funding for comparative-effectiveness research and created an independent entity—the Patient-Centered Outcomes Research Institute (PCORI)—outside the government to oversee this research. The law, while funding new comparative-effectiveness research, explicitly forbids the federal government from using cost-effectiveness estimates in the new research or as the basis for establishing what type of health care is recommended. The law further forbids Medicare decisions based on cost-effectiveness criteria or even using comparative effectiveness “in a manner that treats extending the life of an elderly, disabled, or terminally ill individual as of lower value than extending the life of an individual who is younger, nondisabled, or not terminally ill.” The political minefields represented by these restrictions are an important consideration in any use of comparative effectiveness or cost effectiveness for prescription drug pricing.

Many other nations—especially Australia, Canada, Germany and the United Kingdom—have been less wary of using comparative-effectiveness research or even cost-effectiveness research. Each of these nations has an agency charged with reviewing existing literature and making recommendations for government health programs.40 The National Institute for Health and Clinical Effectiveness (NICE) in the United Kingdom, established in 1999, is probably the most prominent of these agencies, which typically are operated by the government but draw on a variety of experts and have a degree of independence. NICE is governed by a board with members drawn from settings such as academia and public health and practicing physicians, with additional input from an expert methodology committee and a committee of stakeholders, including consumer representatives.

NICE experts evaluate most newly approved drugs and new indications for drugs already on the market through systematic reviews of available research but do not initiate new studies.41 Under its current rules, NICE decides whether to recommend the drug or technology based on its evaluation of the available research. Patients have a constitutional right to receive recommended drugs, and the National Health Service (NHS), the United Kingdom’s universal, public health program, will pay for the drug. Drugs assigned a “not-recommended” status are still available to patients for purchase but are not covered by the NHS. Unlike some other national health systems, neither NICE nor the NHS sets prices for recommended drugs.

The vast majority of drugs or technologies reviewed receive a full recommendation or an optimized recommendation where the drug or technology is recommended for a smaller subgroup of patients than originally requested by the manufacturer. Recommendations rely on a cost-effectiveness threshold, essentially the number of quality-adjusted life-years (QALYs) gained from use of the studied drug at a stated cost. The goal is to maximize the benefit to public health under the available budget. NICE also seeks to account for other social values and information on the public’s values, but such considerations have been difficult. As described by one analyst, NICE must balance, within a fixed budget, the needs of patients who gain from the treatment under consideration at the manufacturer’s price against another unknown set of patients who may fail to get some unknown treatment because money was spent on the treatment being studied.42

Beginning in 2014, the United Kingdom is set to implement a new value-based pricing approach for drugs in place of the current system that seeks to control costs by regulating the profits of pharmaceutical manufacturers. The new system would retain the role of NICE in assessing evidence on relative clinical and cost effectiveness.43 Rather than only making a yes-no recommendation that creates a right of access to a recommended drug, the NHS would negotiate prices with manufacturers. Negotiations would take into account the cost-effectiveness analysis, as well as three newly explicit factors: unmet need for treatment or severity of illness, extent of therapeutic innovation involved, and wider societal benefit. The idea is to negotiate a higher price if one or more of these factors are satisfied. Unlike the U.S. system, the NHS does not propose to change its current policies of flat copayments, regardless of the drug’s price, and no copayments for most purchases.

Use of Clinical Assessments in the United States

The approach to coverage decisions proposed in the United Kingdom appears counter to the principles established for the new comparative-effectiveness research authorized by the health reform law, but U.S. public and private programs already use assessments of a drug’s clinical value. This use occurs primarily in the process of creating formularies or preferred drug lists, together with a process for granting exceptions based on individual patient circumstances.44 Many private health plans and PBMs are active in analyzing or sponsoring comparative-effectiveness research. But, because formulary decisions by private health plans are generally not made in public, it is easier to illustrate the process for state Medicaid programs.

Although Medicaid programs must cover all drugs provided by manufacturers participating in the Medicaid rebate program, states are permitted to employ preferred drug lists. Typically, this means that all drugs are available, but those not on the preferred list require prior authorization. Decisions on which drugs receive preferred status involve both an independent pharmaceutical and therapeutics (P&T) committee and state Medicaid officials. Most states carefully separate cost and clinical considerations in a process where the P&T committee looks only at clinical differences and reports which drugs are clinically superior or equivalent.45

After receiving P&T committee recommendations, state officials look at the cost of drugs viewed as clinically equivalent to the best treatment in the class. In doing so, they have the discretion to base judgments on other criteria. For example, most states have chosen to be more inclusive with mental health drugs on their preferred drug lists, based in part on pushback from patients and providers and in part by the idea that switching among therapy options is more risky for patients taking mental health drugs than with many other drug classes.

Several states use comparative-effectiveness assessments conducted by the Drug Effectiveness Review Project (DERP) at the Oregon Health & Science University. Unlike NICE, the DERP focuses reviews on comparative effectiveness not cost effectiveness. Patient-specific differences are generally handled through state decisions to apply prior authorization or other utilization management criteria, although a DERP literature review might highlight the likelihood of patient-level differences for a particular drug. The procedures used to review various utilization management requests and transparency of the criteria may vary substantially from one state to another.

Options for Using Value-Based Pricing in the United States

As with reference pricing, the use of value-based pricing or other methods that rely on comparative-effectiveness or cost-effectiveness information differs considerably in the U.S. health system from applications in countries that rely heavily on a single national health system. In the United Kingdom, one decision can be made to cover a drug under the NHS or to negotiate a price for NHS use. In the United States, an individual health plan cannot set a retail price but can negotiate for rebates relying on its potential to shift volume to other drugs on the basis of the comparative-effectiveness evidence. Similarly, a plan has the ability to exclude some drugs from its formulary and to provide preferred status to others.

The differences across national settings have effects that cut both ways. In a national health system like the United Kingdom, one decision not to cover a drug shown to be less effective or to negotiate a lower price from the manufacturer can have a substantial effect on total spending or appropriate drug use. By contrast, an array of separate decisions by multiple purchasers or payers in the U.S. system may increase their feasibility by avoiding the market impact on a manufacturer of a single global decision to drop coverage of a drug. A manufacturer whose drug scores less well on comparative effectiveness might still be able set a price above production costs and recoup some of its investment.

The advantage for consumers of a broader role for effectiveness research in formulary and drug benefit design is more credibility and trust for decisions that may otherwise appear to be driven solely by economics. Evidence-based decisions also should increase the alignment between financial incentives and health outcomes achieved through use of the most effective medicines.

Although tiered cost sharing is effectively the industry standard in both private and public sectors in the United States, it is unclear how consistently formulary and tier-placement decisions are linked today to good information on comparative effectiveness or cost effectiveness. Broader availability of unbiased information, such as expected from the PCORI, should help. Although the health reform law stipulates that new information developed by the PCORI cannot be used by the government as mandates, guidelines or policy recommendations or as sole evidence in making Medicare coverage decisions, it presumably can be used as a starting point for price negotiations or other actions by payers, such as formulary decisions and tiered cost sharing approaches. If such information is used more consistently, it could help increase the incentives for manufacturers to develop therapies that make a difference in patient outcomes as opposed to the so-called “me too” drugs that offer little clinical advantage over less-expensive alternatives in a given drug class.

Any PBM, large private health plan or group of plans, such as the Blue Cross Blue Shield Association, could fund its own analysis of comparative effectiveness or cost effectiveness and then use that information to influence its price negotiations and formulary decisions. Or it could draw on available studies funded by the DERP, PCORI or from the general published literature. Some organizations take these steps today. Plans taking steps to use evidence in formulary decisions could emphasize this point in marketing to purchasers and consumers.

These same considerations apply to Medicare drug plans, which are already required by law to use P&T committees and to ensure that committee decisions are based on “the strength of scientific evidence and standards of practice.”46 It is unknown, however, how well this requirement is enforced. Medicare could take additional steps to mandate the use of certain effectiveness (or cost-effectiveness) information for certain drug classes, to establish and disseminate best practices from across the industry, or to use performance measures as a means of increasing plans’ incentives to follow consensus findings on comparative effectiveness in certain drug classes.

As with reference pricing, more use of effectiveness research for formulary decisions or value-based pricing will bring trade-offs. Any use of formularies may be seen by some consumers as a restriction on their access to drugs of choice. As noted in the discussion of reference pricing, the use of consensus scientific evidence helps offer a degree of protection for consumers. Still, it will be critical that effectiveness studies consider the differential effects for relevant subgroups of patients. Furthermore, an accessible exceptions process will remain vital for patients whose individual clinical needs differ from the consensus findings.

Pharmaceutical manufacturers remain concerned that expanded use of comparative-effectiveness and cost-effectiveness research will have an adverse impact on innovation. In their view, the risk that such research will limit access to a new drug before the clinical community gets a full chance to learn about its benefits and risks will curtail research and development efforts. One response is that recent research efforts have focused too much on marginal improvement to existing drugs and that better studies of comparative effectiveness might refocus research more on significant therapy breakthroughs.

Using Evidence to Guide Decisions

In an era when the United States is keenly focused on identifying effective means of controlling health costs without an adverse impact on patients, new ideas for managing drug costs should be highly welcome. Reference pricing is a policy option worthy of consideration by different U.S. payers, at least for some drug classes. Reference pricing strengthens incentives and offers the potential for greater savings through higher use of generics and more cost-effective brand options. But, it also raises some concerns of more constrained choices for patients, as well as an uncertain impact on pharmaceutical research and development.

The comparative-effectiveness or cost-effectiveness research that underlies the new value-based pricing being developed in the United Kingdom would have considerable applicability for U.S. payers as a means of establishing evidence-based support for benefit and formulary designs currently in use or developed in the future.

Notes

1. Martin, Anne, et al., “Growth in U.S. Health Spending Remained Slow in 2010; Health Share of Gross Domestic Product Was Unchanged from 2009,” Health Affairs, Vol. 31, No. 1 (January 2012). Drugs provided as part of a hospital stay or administered by a physician (e.g., chemotherapy infusions) are excluded from these estimates.

2. Keehan, Sean P., et al., “National Health Expenditure Projections: Modest Annual Growth Until Coverage Expands and Economic Growth Accelerates,” Health Affairs, Vol. 31, No. 7 (July 2012).

3. Gellad, Walid F., et al., “The Financial Burden from Prescription Drugs Has Declined Recently for the Nonelderly, Although it is Still High for Many,” Health Affairs, Vol. 31, No. 2 (February 2012).

4. IMS Institute for Healthcare Informatics, The Use of Medicines in the United States: Review of 2011, Parsippany, N.J. (April 2012). Branded generics account for about half of all spending on generics, although probably only about 10 percent of prescriptions.

5.Entry of a second generic competitor is associated with the largest price reduction. There is little reduction (94% of the brand price) with one competitor. With two competitors, the average price is 52 percent of the brand price; with six or more competitors, the price drops to one-fourth. http://www.fda.gov/AboutFDA/CentersOffices/OfficeofMedicalProductsandTobacco/CDER/ucm129385.htm.

6. Generic Pharmaceutical Association, Savings—$1 Trillion Over 10 Years: Generic Drug Savings in the U.S., Washington, D.C. (August 2012).

7. Congressional Budget Office, Effects of Using Generic Drugs on Medicare’s Prescription Drug Spending, Washington, D.C. (September 2010).

8. Haas, Jennifer S., et al., “Potential Savings from Substituting Generic Drugs for Brand-Name Drugs: Medical Expenditure Panel Survey, 1997-2000,” Annals of Internal Medicine, Vol. 142, No. 11 (June 7, 2005); Donohue, Julie M., et al., “Sources of Regional Variation in Medicare Part D Drug Spending,” New England Journal of Medicine, Vol. 366, No. 6, (Feb. 9, 2012).

9. IMS Institute for Healthcare Informatics, The Use of Medicines in the United States: Review of 2010, Parsippany, NJ. (April 2011). Exceptions may exist for some narrow therapeutic index drugs.

10. Grossman, Joy M., et al., Physician Practices, E-Prescribing and Accessing Information to Improve Prescribing Decisions, Research Brief No. 20, Center for Studying Health System Change, Washington, D.C. (May 2011).

11. This state of affairs reflects the confluence of two trends an increased number of Americans who have some form of insurance for their drug purchases, together with a shift toward point-of-purchase transactions for those with coverage. IMS Institute for Healthcare Informatics, The Use of Medicines in the United States: Review of 2011, Parsippany, N.J. (April 2012).

12. Office of the Assistant Secretary for Planning and Evaluation (ASPE), Expanding the Use of Generic Drugs, Washington, D.C. (Dec. 1, 2010).

13. Shrank, William H., et al., “State Generic Substitution Laws Can Lower Drug Outlays under Medicaid,” Health Affairs, Vol. 29, No. 7 (July 2010).

14. Kaiser Family Foundation, Menlo Park, Calif., and Health Research & Educational Trust, Chicago, Ill., Employer Health Benefits 2011 Annual Survey (September 2011); Hoadley, Jack, et al., Medicare 2011 Part D Data Spotlight: Analysis of Medicare Prescription Drug Plans in 2011 and Key Trends Since 2006, Issue Brief No. 8237, Kaiser Family Foundation, Menlo Park, Calif. (September 2011).

15. O’Malley, A. James, et al., “Impact of Alternative Interventions on Changes in Generic Dispensing Rates,” Health Services Research, Vol. 41, No. 5 (October 2006).

16. Other approaches are possible. Washington’s Medicaid program allows pharmacists to substitute a drug from the Medicaid preferred drug list for a prescribed nonpreferred drug without specific permission from those physicians who participate in the program. Bergman, David, et al., State Design and Use of Prior Authorization Processes, Issue Brief, National Academy for State Health Policy, Portland, Maine (March 2006). Also, recent legislation in two Canadian provinces provides pharmacists an expanded scope of practice to carry out therapeutic substitutions; a regional Blue Cross plan implemented a pilot program in 2011 that monitor its use. LePage, Suzanne, “Therapeutic Substitution: Will It Yield Benefits for Drug Plan Sponsors?” Benefits Canada (Dec. 9, 2011).

17. Shrank, William H., et al., “Patients’ Perceptions of Generic Medicines,” Health Affairs, Vol. 28, No. 2 (March/April 2009).

18. Kesselheim, Aaron S., et al., “Clinical Equivalence of Generic and Brand-Name Drugs Used in Cardiovascular Disease,” Journal of the American Medical Association, Vol. 300, No. 21 (Dec. 3, 2008).

19. Steinman, Michael A., Mary-Margaret Chren and C. Seth Landefeld, “What’s in a Name? Use of Brand versus Generic Drug Names in United States Outpatient Practice,” Journal of General Internal Medicine, Vol. 22, No. 5 (May 2007); Fischer, Michael A., et al., “Effect of Electronic Prescribing with Formulary Decision Support on Medication Use and Cost,” Archives of Internal Medicine, Vol. 168, No. 22 (Dec. 8, 2008).

20. Pham, Hoangmai H., G. Caleb Alexander and Ann S. O’Malley, “Physician Consideration of Patients’ Out-of-Pocket Costs in Making Common Clinical Decisions,” Archives of Internal Medicine, Vol. 167, No. 7 (April 2007); Alexander, G. Caleb, et al., “Patient-Physician Communication about Out-of-Pocket Costs,” Journal of the American Medical Association, Vol. 290, No. 7 (Aug. 20, 2003); Korn, Lisa M., et al., “Improving Physicians’ Knowledge of the Costs of Common Medications and Willingness to Consider Costs When Prescribing,” Journal of General Internal Medicine, Vol. 18, No. 1 (January 2003); Reichert, Steven, et al., “Physicians’ Attitudes about Prescribing and Knowledge of the Costs of Common Medications,” Archives of Internal Medicine, Vol. 160, No. 18 (October 2000).

21. The pattern is different in closed systems, such as the Department of Veterans Affairs or integrated health plans (such as Kaiser Permanente) where the formulary is viewed as a tool of physicians rather than being enforced at the point of sale by the health plan. In these settings, physicians may be involved in decisions about what drugs are listed on the formulary and tend to prescribe these drugs unless an alternative is suggested by a particular patient’s circumstances.

22. Brekke, Kurt R., Ingrid Königbauer and Odd Rune Straume, “Reference Pricing of Pharmaceuticals,” Journal of Health Economics, Vol. 26, No. 3 (May 2007); Galizzi, Matteo Maria, Simone Ghislandi and Marisa Miraldo, “Effects of Reference Pricing in Pharmaceutical Markets: A Review,” Pharmacoeconomics, Vol. 29, No. 1 (January 2011). Two countries (Norway and Sweden) have recently dropped use of reference pricing since the time of the reviewed studies.

23. Kanavos, Panos and Uwe Reinhardt, “Reference Pricing for Drugs: Is It Compatible With U.S. Health Care?” Health Affairs, Vol. 22, No. 3 (May/June 2003).

24. Claxton, Gary, et al., Employer Health Benefits 2011 Annual Survey, Pub. No. 8225, Kaiser Family Foundation, Menlo Park, Calif., and Health Research & Educational Trust, Chicago, Ill. (2011). For some examples of U.S. health plans using reference pricing, see Edlin, Mari, “Reference-Based Pricing Levels Out Drug Spending for Employers,” Managed Healthcare Executive (June 1, 2004).

25. Towers Watson, New York, N.Y., and National Business Group on Health, Washington, D.C., Performance in an Era of Uncertainty: 17th Annual Towers Watson/National Business Group on Health Employer Survey on Purchasing Value in Health Care (2012).

26. Centers for Medicare & Medicaid Services, 2010 Combined Call Letter, Baltimore, Md., (March 30, 2009).

27. Galizzi, Ghislandi and Miraldo (2011).

28. Ibid.

29. Morgan, Steve, Gillian Hanley and Devon Greyson, “Comparison of Tiered Formularies and Reference Priding Policies: A Systematic Review,” Open Medicine, published online (Aug. 4, 2009).

30. Medicare is Australia’s publicly funded universal health care system; the PBS, although technically separate, is operated by the same agency as Medicare. Medicare provides health services to most citizens and permanent residents, although many also obtain private insurance.

31. Reforms in 2007 changed incentives for achieving lower generic prices by creating a separate formulary for drugs with generic competition and requiring price reductions for drugs on that formulary. Department of Health and Ageing, Strengthening Your PBS—Preparing for the Future, Canberra, Australia (Nov. 16, 2006); Bulfone, Liliana, “High Prices for Generics in Australia—More Competition Might Help,” Australian Health Review, Vol. 33, No. 2 (May 2009); Lofgren, Hans, “Generic Medicines in Australia: Business Dynamics and Recent Policy Reform,” Southern Med Review, Vol. 2, No. 2 (September 2009).

32. Pharmaceutical Benefits Pricing Authority, Department of Health and Ageing, Annual Report for the Year Ended 30 June 2006, Canberra, Australia (2006).

33. Johnson, Jill T., Kathryn K. Neill, and Dwight A. Davis, “Five-Year Examination of Utilization and Drug Cost Outcomes Associated with Benefit Design Changes Including Reference Pricing for Proton Pump Inhibitors in a State Employee Health Plan,” Journal of Managed Care Pharmacy, Vol. 17, No. 3 (April 2011).

34. This example is unusual in having an over-the-counter product establish the reference price, but the principle would be the same for other examples.

35. Use of reference pricing at the national level in the United States would also imply a broader set of changes to insurance coverage for drugs.

36. Recently, some manufacturers have taken steps seeking to preserve market share for brand-name drugs after patent expiration, as illustrated by Pfizer’s efforts to protect Lipitor with consumer coupons and apparent deals with PBMs to keep out-of-pocket costs at a level comparable to the new generic versions. Wilson, Duff, “Facing Generic Lipitor Rivals, Pfizer Battles to Protect Its Cash Cow,” New York Times (Nov. 29, 2011).

37. A recent study offers evidence that new users of brand and generic antidepressants were equally likely to remain on therapy, and average costs (both drug costs and other health costs) were lower for those on generic drugs. Vlahiotis, Anna, et al., “Discontinuation Rates and Health Care Costs in Adult Patients Starting Generic Versus Brand SSRI or SNRI Antidepressants in Commercial Health Plans,” Journal of Managed Care Pharmacy, Vol. 17, No. 2 (March 2011).

38. Galizzi, Ghislandi and Miraldo (2011).

39. Comparative-effectiveness research seeks to determine the relative effectiveness of different drugs in terms of health care outcomes and quality. Cost-effectiveness research adds a cost or value component, usually comparing the cost of achieving a unit of health benefit, such as an extra year of life or quality-adjusted year of life. See Gluck, Michael E., Incorporating Costs into Comparative Effectiveness Research, Research Insights, AcademyHealth, Washington, D.C. (May 2009).

40. For overviews, see Chalkidou, Kalipso, and Gerard Anderson, Comparative Effectiveness Research: International Experience and Implications for the United States, Research Insights, AcademyHealth, Washington, D.C. (July 2009); Keckley, Paul H., et al., Comparative Effectiveness Research in the United States, Issue Brief, Deloitte Center for Health Solutions, Washington, D.C. (May 2011); Chalkidou, Kalipso, et al., “Comparative Effectiveness Research and Evidence-Based Health Policy: Experience from Four Countries,” Milbank Quarterly, Vol. 87, No. 2 (June 2009).

41. Faden, Ruth R., and Kalipso Chalkidou, “Determining the Value of Drugs—The Evolving British Experience,” New England Journal of Medicine, Vol. 364, No. 14 (April 7, 2011); Chalkidou, Kalipso, Comparative Effectiveness Review Within the U.K.’s National Institute for Health and Clinical Effectiveness, Issue Brief, Commonwealth Fund, New York, N.Y. (July 2009).

42. Towse, Adrian, ”Value Based Pricing, Research and Development, and Patient Access Schemes. Will the United Kingdom Get it Right or Wrong?“ British Journal of Clinical Pharmacology, Vol. 70, No. 3 (September 2010).

43. Faden and Chalkidou (2011); Towse (2010); Claxton, Karl, Mark Sculpher, and Stuart Carroll, Value-Based Pricing for Pharmaceuticals: Its Role, Specification and Prospects in a Newly Devolved NHS, CHE Research Paper No. 60, University of York Centre for Health Economics, York, United Kingdom (February 2011).

44. See also the discussion in Gluck (2009).

45. Bergman, David, et al., Using Clinical Evidence to Manage Pharmacy Benefits: Experiences of Six States, Issue Brief, Commonwealth Fund, New York, N.Y. (March 2006).

46. Medicare Prescription Drug, Improvement, and Modernization Act of 2003, Public Law No. 180-173, Sec. 1860D-4(b)(3)(B)(i) (Dec. 8, 2003).

About the Author

Jack Hoadley, Ph.D., is a research professor at Georgetown Univerity’s Health Policy Institute.